Send this article to a friend:

February

27

2026

|

Send this article to a friend: February |

HALO: The Great Rotation Has Begun

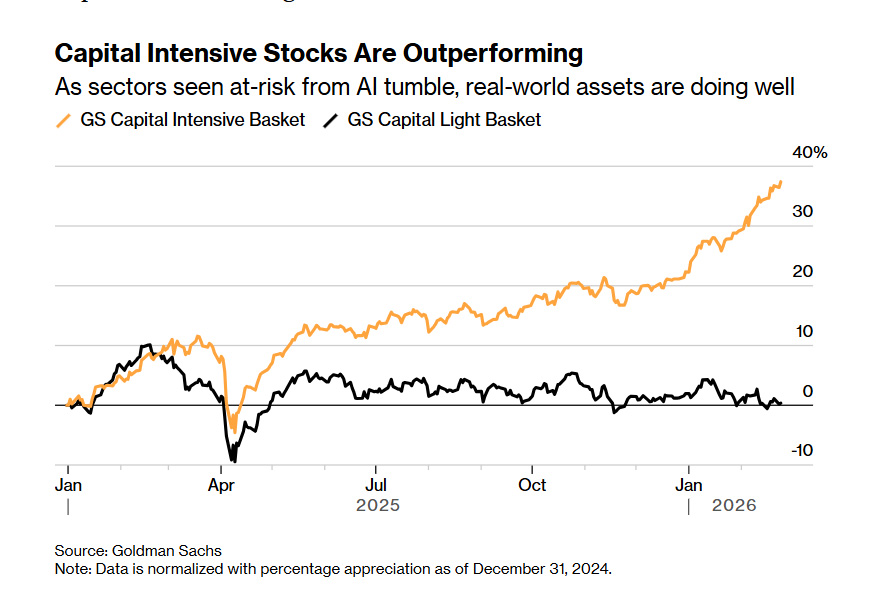

Software is the poster boy here. The sector was attractive because once you build a software product, it doesn’t cost much to onboard new customers. There’s no physical cost to create a new software license. It’s all done in the cloud these days. So once a software business gets cranking, the recurring revenue and profits can be extremely lucrative. But investors went overboard, bidding up these names to silly valuations. Meanwhile, companies that run capital-intensive businesses, like oil majors, railroads, and gold miners were seen as dinosaurs. But now the script has flipped. Asset-light stocks are seen as vulnerable to AI disruption. And too expensive. We’re seeing this most clearly in the current software meltdown. Even software king Microsoft is down 27% from its highs. And many smaller software-as-a-service (SaaS) companies are getting hit much worse. Monday.com (MNDY), a former high-flyer, is down 75% over the past year. Figma (FIG) is down 78%. There are dozens of these examples out there. A HALO Around Hard Assets But capital-intensive businesses are shining. Companies that own large mines, oil fields, and refineries have risen significantly over the past year. A new acronym has been created to describe this shift: HALO. It stands for Heavy Asset Low Obsolescence. The focus is on stocks that won’t be disrupted by AI, and should weather inflation well. See the chart below, via Bloomberg and Goldman Sachs. It shows how Goldman’s “capital intensive” index has outperformed the “capital light” index by nearly 40%.

These types of assets are very expensive to replicate. Sometimes even impossible. For example, one of the hottest sectors today is utilities. The companies that make our electricity. Building new power plants and grid infrastructure is extremely difficult. Nobody wants a new power plant in their neighborhood, so there is naturally a premium being put on existing assets. Utilities are at all-time highs today. They’re printing money from increased demand for electricity thanks to the data center boom. And the lack of new competitors doesn’t hurt. Eventually ,we will get some new power generation online here in the U.S. But it’s going to take a long time, and AI data centers will gladly gobble all that new power up. Miners, Drillers, and EMUtilities are an interesting way to play the HALO effect. But I suspect the government may crack down on their profit-making eventually. Consumers are being gouged by electricity prices today, due to all the new data centers. And while I suspect part of the solution will be higher prices for big tech, it’s also possible that governments crack down on utility profits. So our focus will continue to primarily be on miners, drillers, and cheap emerging market stocks. The world has underinvested in these assets for decades, and now the tide is finally turning. Acronyms Drive Capital Remember the BRICS investment craze? FAANG? These were powerful narratives that helped steer investment into specific areas. So while HALO may seem like just another acronym, I view it as an important development. It is an acknowledgement by Wall Street of what we here at Paradigm have been talking about for the past few years. Capital is rotating out of soft tech stocks, and into hard assets. People want the surety that only big mines, large factories, oil fields, and other physical assets can bring. Recent developments in AI have introduced unique risks to tech firms. It’s never been this easy to create custom software using AI tools. While in the short-term, fears may be overdone, in the long run we’re on course for serious disruption in the tech world. If AI models like Anthropic’s Claude continue to improve, many companies will develop their own internal solutions and eliminate the need for countless software products. This AI disruption is happening at the same time as we’re entering what is likely to be an inflationary period, and the beginning of a new commodity boom. This makes getting exposure to natural resources and HALO assets an imperative for all investors. I believe this trend will continue for years to come. Instead of high-margin software businesses, investors will shift into natural resources. Companies with lots of revenue, relatively small margins, and valuable asset bases. Companies that aren’t threatened with disruption by fast-advancing AI models. And ones that will thrive if we do enter another inflationary period. Our goal over the coming weeks and months is to present ideas to help prepare your portfolio for this shift.

Adam Sharp has been a financial writer and Fed watcher since 2008. He is a contrarian who specializes in non-traditional assets. Adam founded and sold Early Investing, a newsletter about alternative investments. Sharp lives in Maryland with his wife, two children, and two dogs.

|

Send this article to a friend:

|

|

|

For the past 15 years, investors have crowded into “capital light” stocks.

For the past 15 years, investors have crowded into “capital light” stocks.